Orient Bell: What is wrong when everything is right?

A history lesson, the pick of the picky, the path to supernormal, missed opportunities and a metamorphosis

Today we cover a business which is sitting on large capacities with cost-efficiencies, waiting for demand to turn. The downside is, you could be sitting on dead money for longer than you can anticipate. The company’s name is Orient Bell.This is no recommendation to buy or sell.

A History Lesson(Again)

Starting in 1451, Mehmud-II set out to do the unthinkable. He built out massive cannons, positioned supply chains and waited for the Byzantine empire to tire out in the search for one thing– an opportune moment- a moment which he believed with his capabilities would lead to the fall of the city of Constantinople.

The preparations were in the works for two full years before the eventual attack, but funnily enough nobody noticed. Why? The answer is miserably simple-everybody dismissed the actions of Mehmud-II as mere posturing. How could something which had not happened in a 1000 years happen all at once? How can a major city crumble at the hands of a marauder? How could somebody outshine when they hadn’t done it in the past?

But perhaps more interestingly, if there were markets back then- I’m pretty sure people wouldn’t have been interested in Mehmud’s preparation in search for the perfect moment. Because it’s never been that cool to understand and look at what is right in front of you. The most brilliant ideas are brilliant because they hit you right in the middle of your eyes.

Humans love narratives. They love “AI is changing everything” or “EV revolution” or “China+1 opportunity.” These are stories you can tell at a dinner party and sound smart.

“I bought a tile company waiting for their cycle to turn” doesn’t have the same ring to it.

But who cares about parties after all?

The Pick for the Picky

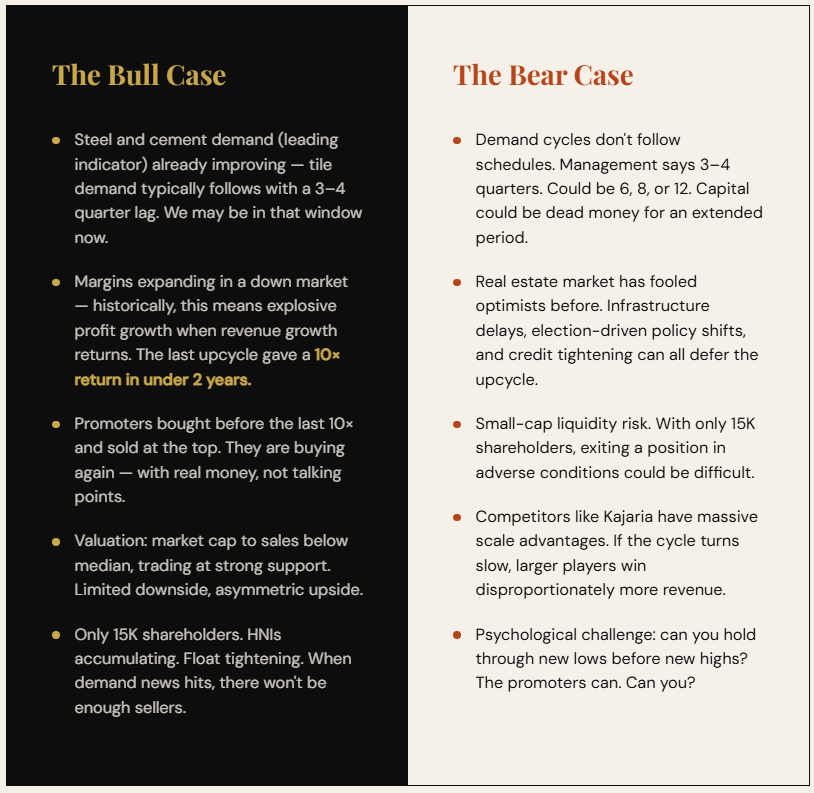

Orient Bell has the following characteristics:

Rising promoter holding every quarter

Rising margins due to operating efficiencies

New product launches- tile adhesives

Low equity base of <1.5 Cr shares traded

Is trading at a strong support

Market cap to sales at lower than median

An excellent and focused management team

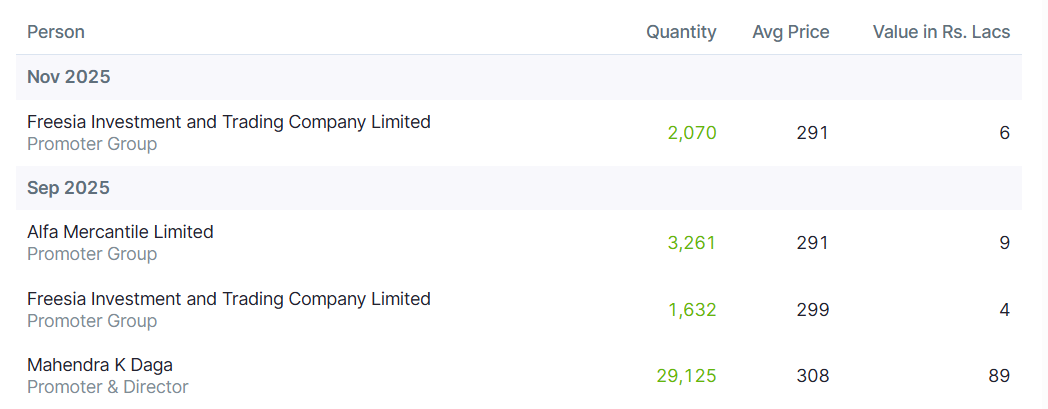

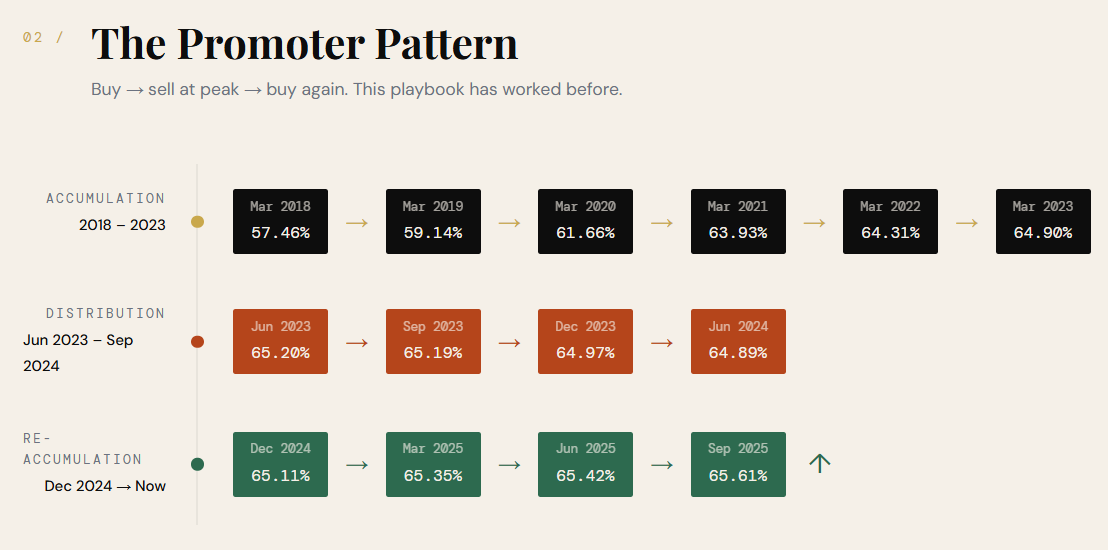

Added to this, the last time there was an upcycle, the business gave a 10X return in less than 2 years. But more interestingly the promoters were buying in the lead up to this move too, and sold after the up move.

The buying over years:

And the selling starting Jun 2023

Guess what has been happening since Dec 2024 qtr

And what hasn’t stopped post Sept, 2025

If you analyse the shareholding pattern further, you’ll realise the HNIs are accumulating too. Shareholders are going down every quarter as the few hands roll-up the shares. It only has 15K shareholders in any case, so it makes it even more interesting.

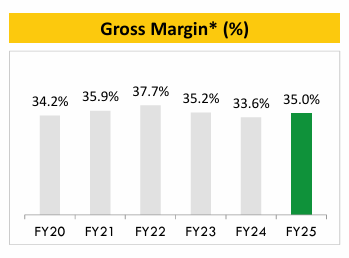

This is just shareholding, which doesn’t actually mean anything beyond a point, the interesting thing about the business is playing out in its margins.

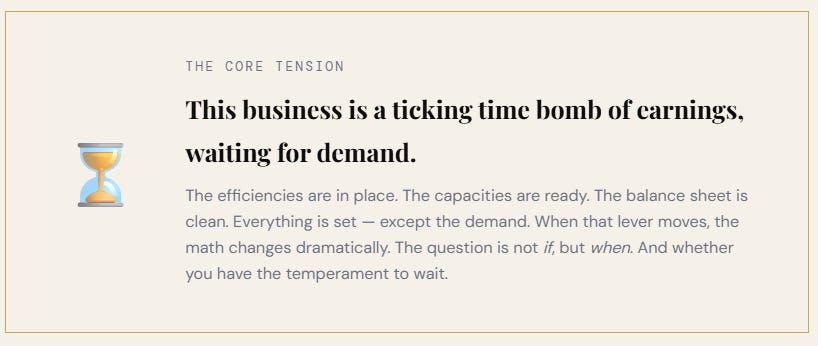

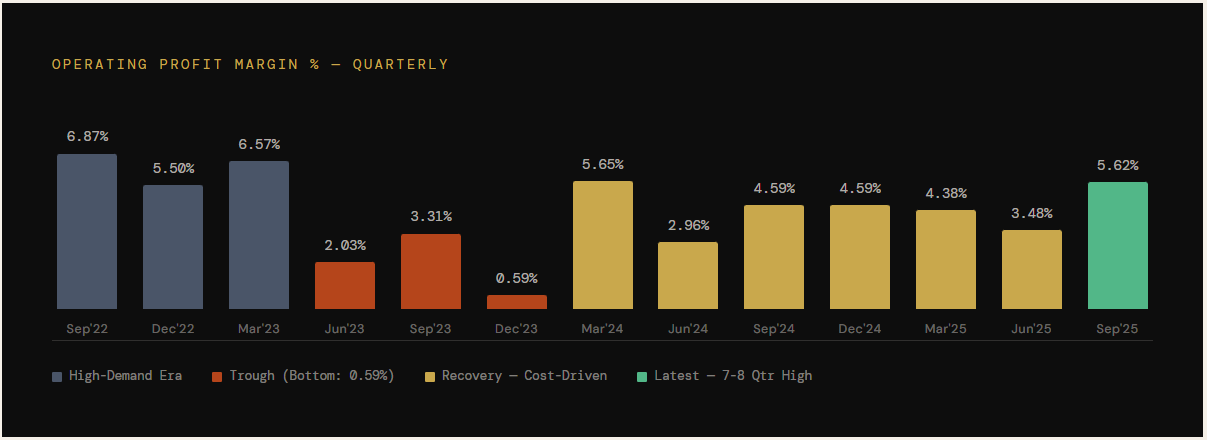

The path to the super-normal

See the gradual increase in margins post Sep 2024? The margins bottomed out around 0.59% to reach here. You’ll look at the Sep 2022 quarter and say this isn’t enough, but I’ll tell you that the Sep 2022 quarter was one of very large demand, demand is subdued right now- the sales in Sep 2025 were lower than Sep 2022, but margins have increased only due to the cost saving exercises done.

In the Dec 2025 quarter, the company delivered the highest margins of the past 7-8 quarters and the management said they would expect this trend to continue and in fact get better in the coming quarters. Something beautiful is happening in Orient Bell without a demand uptick. Imagine if that lever moves too.

This business is a ticking time bomb of earnings waiting for demand to come- the efficiencies are in place, as evidenced by the margins, the capacities are in place- as evidenced by the 70 Cr increase in fixed assets from the last upcycle of 2022, and there’s no debt on the balance sheet.

But why exactly isn’t there more interest for the business? One, great investments are never advertised and two, it might be wise for me to tell you about their history.

On Missed Opportunities

Vijay Kedia sir famously says that “One Stock can change your life”, the example he gives for this is Cera Sanitaryware, a company which went up 16000 times for him(adjusted for dividends). It’s a very inspiring story of wealth creation over 18 years and you should listen to it.

But essentially, he bought the company at a market cap of about 64 Lakh in 2005 and sold it in 2023 at a market cap of around 10,311 Cr. I wish I was active in the times when companies were trading for 64 Lakh Mcap! Adjusted for inflation today, this can be calculated as being between 1.69 Cr to 2.30 Cr. So if you want to see returns of this kind, buy stuff at this price!

But I’m mentioning Cera here because companies like Cera and Kajaria which came from the building material space were largely dismissed earlier because this industry sees cash transactions. But these companies have done really well over the past 15 years overcoming multiple issues.

You can clearly see they have acquired large scale with the sales per quarter numbers, leaving Orient Bell far behind.

This is primarily because Orient Bell missed out on every large upcycle before this. There were four reasons for this:

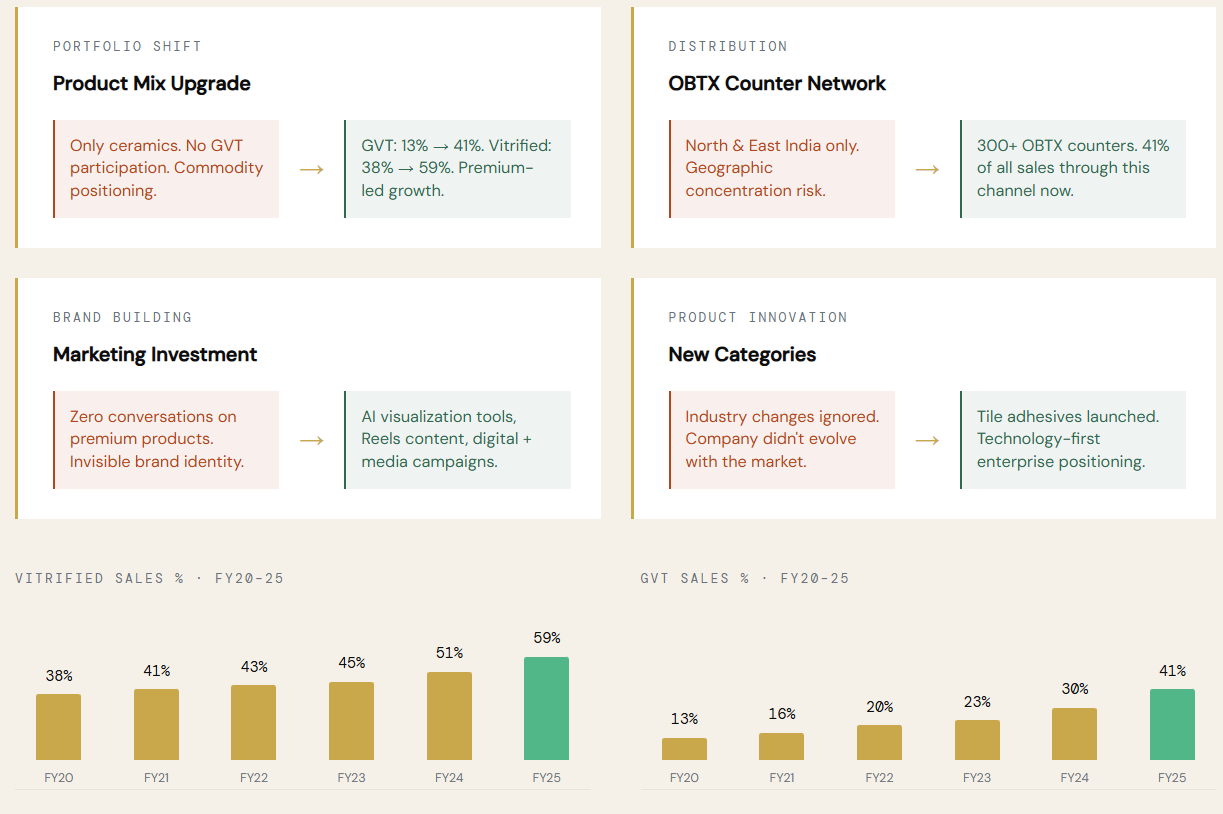

a. They were present only in North and East India and missed out on the South and West regions because of this.

b. They focused exclusively on ceramic tiles and didn’t participate in the GVT segment

c. Conversations on premium products and branding were entirely absent

d. No conversations on newer changes in the industry took place- the company didn’t evolve as much.

The Metamorphosis

As I’ve mentioned before, a company’s performance can often be tied to the performance of promoters and management teams. Something clicked 5-6 years back when Madhur Daga, one of the promoters decided to step away from day to day operations. (Madhur has done really well with his personal life and fitness though- with Vipassana and Running- you can check his work out here.)

To ensure the previous mistakes were rectified, they brought on board Aditya Gupta to the management team in March 2018. Aditya is a fascinating character, he’s an IIT-IIM professional who has worked in sales and marketing across Telecom, Power and Alcobev. He was serving as the CBO of Tata Power when he was brought in to lead this company out of its problems.

Aditya set out to achieve his mission of bringing great glory to India’s oldest tile manufacturer by focusing on a four pronged strategy:

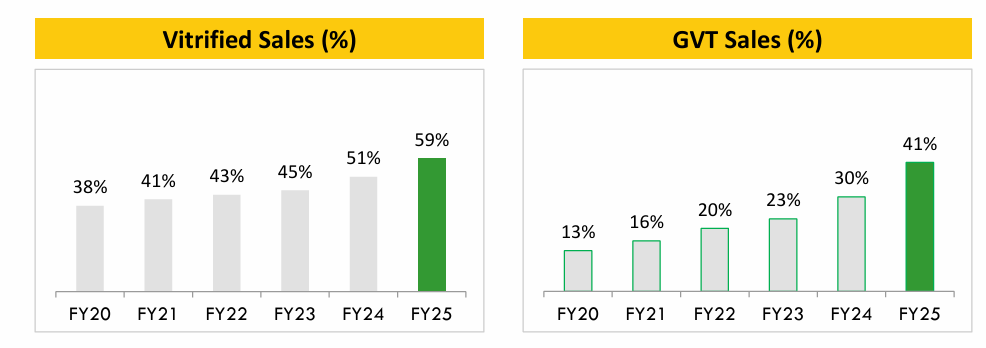

a. Changing product portfolio: higher GVT and Vitrified tiles contribution, this can be evidenced below

b. Offering new channel by creating the OBTX counters

c. Branding and Advertising efforts- focusing on digital and media outlets

d. Leading efforts to create Orient Bell, a technology first enterprise.

All of these have made Orient Bell a very different company from what it was when everything started off.

The thesis on the company can be summarised as in the visual below:

What can spoil our party- the Anti Thesis

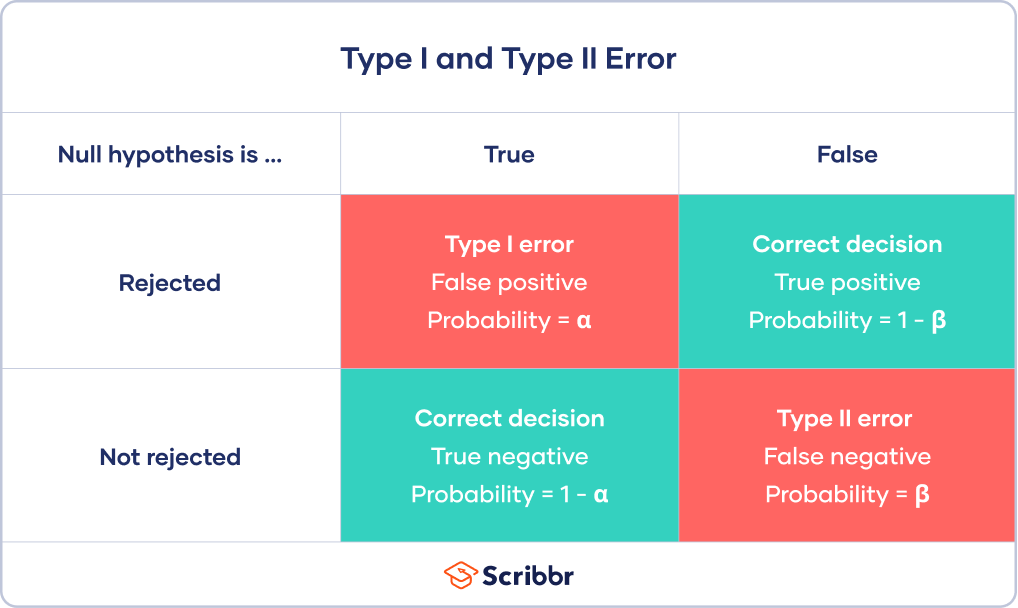

Type-1 errors and type-2 errors have very different consequences for a person. It sounds very smart to dismiss the people who missed out on Mehmud-II’s moves, but one must also realise that missing out on it did not lead to an erosion in capital.

But if somebody had bet on such a change and it wouldn’t have happened, the consequences would have been really large.

So the bear case is all about the wait. How long will we be sitting on dead money with this company.